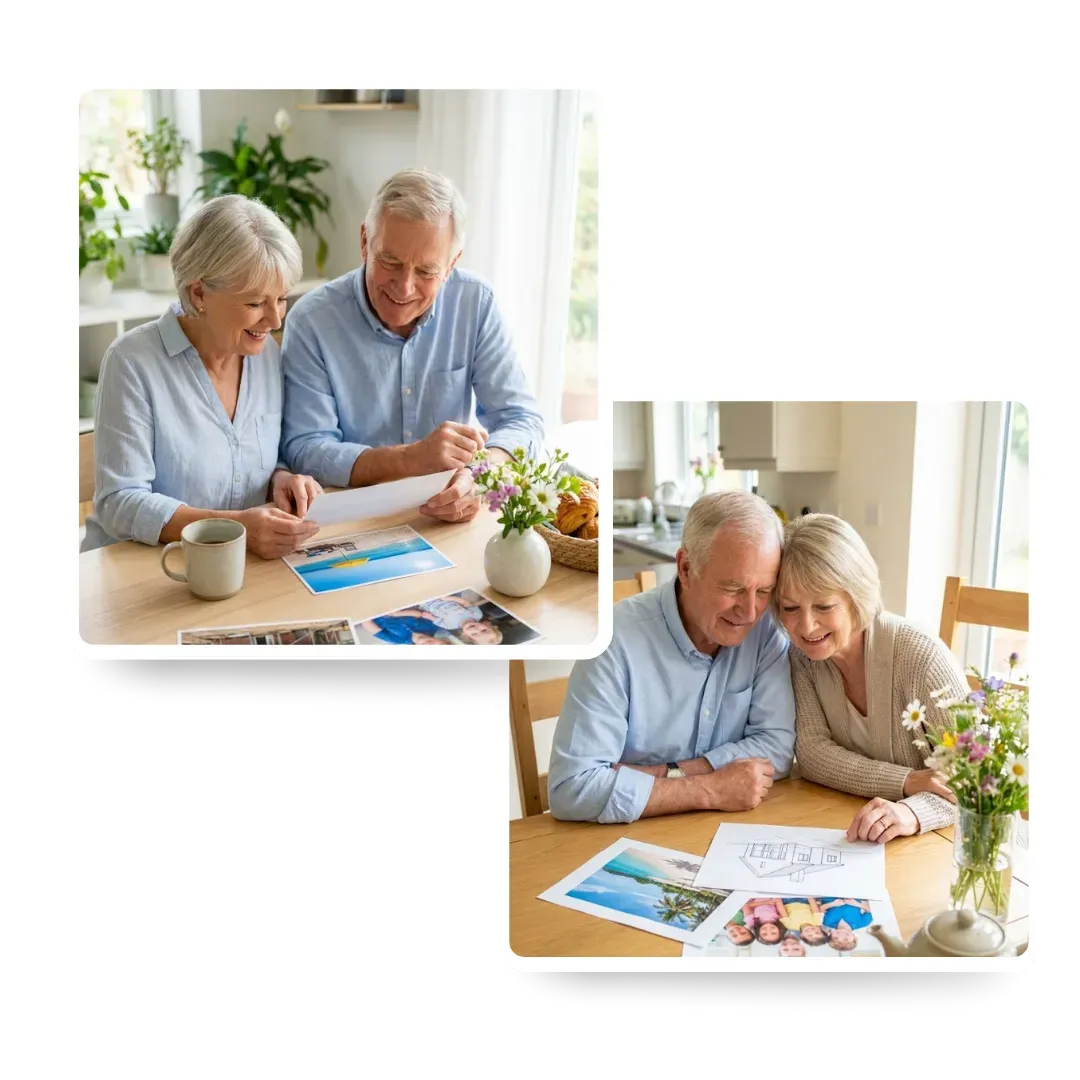

Weighing Up Your Options

Is Equity Release the Right Choice for You?

Equity release is not one size fits all. We help you explore how it could fit with your lifestyle goals and future plans ensuring you make a decision you are comfortable with.

What Can Equity Release Be Used For?

It is about freedom. Access the wealth tied up in your home without moving to fund your retirement goals.

For many people it is a way to improve day to day finances in later life whether that means supplementing your retirement income clearing an existing mortgage or covering rising household costs.

Others use it to fund one off expenses like home improvements a new car or long overdue travel plans. It can also be a way to help loved ones while you are still here to see the difference such as gifting a deposit to children or grandchildren.

However you choose to use the money equity release is a flexible financial tool that should always be considered with your long term plans in mind.

Home Improvements

Boosting Income

Travel & Leisure

Gifting to Family

Equity Release Eligibility Criteria

The basic criteria you need to meet to qualify for most equity release plans.

Homeowner

You must own a property in the UK that is your main residence.

Age 55+

You must be at least 55 years old. For joint applications the youngest applicant must be 55.

Value £70k+

Your property typically needs to be worth at least £70,000.

Every case is assessed individually. Even if you are not sure you meet all requirements it is worth speaking to an adviser.

Are There Alternatives to Equity Release?

Equity release isn't the only way to unlock money in later life, and it is important to consider all your options before making a decision.

Downsizing

Some people choose to downsize to a smaller or more affordable property, which can release capital without taking on any debt.

Savings & Assets

Depending on your goals, using existing savings investments or even local authority grants might also be worth exploring.

Family Support

Others may be able to get financial support from family, whether as a gift or a private arrangement.

Impact of Equity Release on Inheritance

Effect on Your Estate

The loan is repaid from the sale of your home usually after you pass away. This reduces what is left for your loved ones. However plans with Inheritance Protection let you ring fence a portion of value to guarantee a legacy.

Talking to Family

It is a big decision so we actively encourage family involvement. Sharing your plans openly helps avoid misunderstandings. You are welcome to bring relatives to appointments.

Why Independent Equity Release Advice Matters

Equity release can be a valuable financial tool but it is not right for everyone. The best way to find out if it suits your needs is to speak with a qualified adviser who takes the time to understand your goals.

Why Choose Aspect Mortgages?

Independent & Fully Regulated

No Pressure No Jargon

We explore all alternatives first

Get the right advice and the confidence that comes with it

Take the first step towards financial clarity today. There is no obligation and no pressure. Just a friendly conversation to answer your questions.

Fees

A Lifetime Mortgage may reduce the value of your estate and could affect your entitlement to benefits. To understand the features and risks please ask us for a personalised illustration.

There will be a fee for mortgage advice. The precise amount will depend upon your circumstances but we estimate that it will be £1495 for an equity release/retirement mortgage.

Important Information

Aspect Mortgages Limited is authorised and regulated by the Financial Conduct Authority and is entered on the Financial Services Register (https://register.fca.org.uk/s/) under reference 305352. The FCA do not regulate Business Buy to Let Mortgages or Estate Planning.

As independent advisers we have access to the whole market, except for deals that you can only obtain by going direct to a lender. Registered in England and Wales No: 051013801. 16 St Thomas' Road, Chorley, PR7 1HR.

Your home may be repossessed if you do not keep up repayments on your mortgage.

© Copyright 2026 Aspect Mortgages Limited